Have you seen a must-have farm come up for sale only to wonder, “Can I afford it?” Knowing what you can afford today is key to making sure you’re ready for the next time land comes up.

Working with your banker, here are three questions you’ll need to answer before entering a purchase agreement:

1. CAN MY OPERATION SERVICE MORE DEBT?

First determine whether your operation’s recurring cash flows can service additional debt payments across a range of market conditions. The clearest financial metric to show this is your operation’s Debt Service Coverage Ratio (DSCR), which divides your net operating income by the sum of your annual debt payments – both principal and interest.

Lenders typically require a DSCR of 1.2, which ensures that you have a safety cushion to meet your debt obligations as market conditions change.

- If your operation’s DSCR is greater than 1.2, you may be in a position to take on more debt.

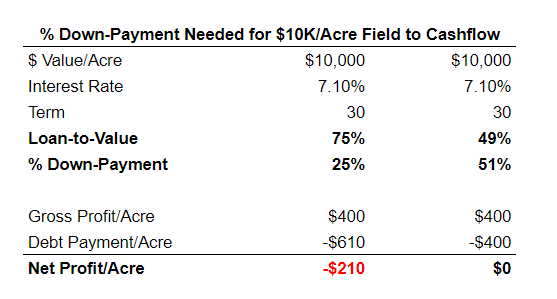

- Likewise, if your DSCR is closer to 1.2, you need to ensure that the parcel you want to buy can cash-flow – meaning its expected profit can cover its debt payments. Making a parcel cash flow will come at the cost of a higher down payment, so you can reduce the debt payments. See the example of buying a $10,000/acre parcel below:

2. DO I HAVE ENOUGH INVESTABLE CAPITAL?

Coming up with a down payment is always a challenge, especially just before harvest when working capital is tight and land starts coming for sale. Determining your investable capital is simply a function of how many liquid assets you have after accounting for your operating expenses and other liabilities through the end of the year.

You can quickly determine this by calculating your Current Ratio, which is your current assets divided by your current liabilities. Lenders typically want to see a ratio of 1.2 to 1.3 to ensure you have a buffer of assets to cover your outstanding expenses and debt payments. Any assets you have over this threshold can be reinvested back into your operation.

3. WHAT’S THE COST OF ACCESSING INVESTABLE CAPITAL WHEN YOU NEED IT?

Timing is never perfect and your investable capital will fluctuate substantially throughout the season. You can avoid being cash-poor through a number of tools including using an operating note, refinancing existing debt, or pulling in outside investors.

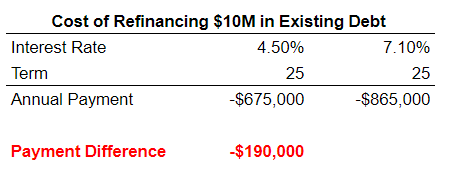

However, these options come with real costs that can stunt your growth long-term if not taken into consideration. For example, refinancing $10 million in existing debt from a 4.5% to 7.1% interest rate could mean $150K+ in new annual debt payments over a 25+ year period.

Are you CAPITAL CONSTRAINED?

Access the capital locked in your land without refinancing through Fractal, a long-term investment partner that co-invests in your land while keeping you in control of how you farm. Learn more

Note this is not investment advice. The information contained should be used for informational purposes.

Authors:

Harrison Rogers is the Marketing Lead at Fractal Agriculture

Steve Conaway is a real estate appraiser and analyst, and farmer of corn, beans, wheat, and grain sorghum in north Kansas

LEARN HOW TO UNLOCK YOUR EQUITY

"*" indicates required fields

We hold your data in high regard. By submitting this form, you are consenting to the use of this information in compliance with our Privacy Policy.